No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.

Over the past five years, the median home value for the state of Washington increased from $421,388 to $603,837. That’s an increase of 43%.

As a result of this trend, many homeowners in Washington currently have a lot of equity that they could tap for other uses, such as home renovations, college tuitions, etc.

The question is, what’s the best option when it comes to tapping your home equity in Washington?

This guide answers a common question among homeowners who find themselves in this situation: “Should I choose a mortgage refinance or home equity loan in Washington?”

Despite having different financial situations, homeowners usually arrive at this decision point for the same reason. They’ve built up significant equity in their homes over the years, and they now want to convert some of it to cash.

Equity growth happens as a result of regular mortgage payments and, in this case, rising home values. Homeowners in Washington who purchased a home a few years ago might currently have 30% to 50% equity—or even more.

When those homeowners seek ways to tap into their equity, they often come to the same fork in the road. Should I refinance my mortgage in Washington to pull cash out, or use a home equity loan instead?

Each option has its own costs, risks and benefits. So knowing how they differ can save you money and headaches down the road.

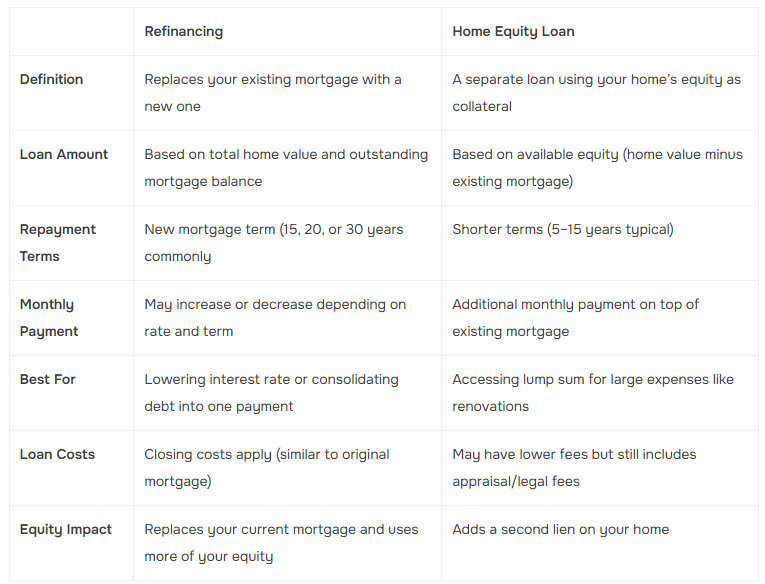

Mortgage refinancing involves taking out a new mortgage loan to replace your existing one. The new loan pays off the old one, and you’re left with a new set of terms.

Under the right circumstances, you can take advantage of the following refinance benefits in WA:

If interest rates have fallen since you took out your original mortgage, refinancing into a lower rate could significantly reduce your monthly payments. You’ll also pay less interest over the long term.

Some homeowners choose to refinance into a shorter loan term, such as going from a 30-year to a 15-year mortgage. While this usually leads to a larger monthly payment, you could pay off your mortgage faster and save substantially on interest in the long run.

With a cash-out refinance in Washington, you can access your home equity. You take out a new mortgage for a larger amount than your current balance. The excess funds are then provided to you in cash, which you can use for various purposes.

Refinancing also allows you to switch from an adjustable-rate mortgage (ARM) to a more predictable fixed-rate mortgage, providing stability in your monthly payments.

With a cash-out refi, everything is wrapped into the new mortgage loan. So you’ll only have to keep track of one payment (versus taking on an additional payment with a home equity loan).

Homeowners in Washington who have significant equity built up could also use a fixed-rate home equity loan in WA to pull cash out of their properties.

Also known as a second mortgage, a home equity loan allows you to borrow a lump sum of money secured by your home’s equity. You receive the full loan amount upfront and then make fixed monthly payments over a set period.

Unlike the refinancing option discussed earlier, this option does not replace your existing mortgage. Your original mortgage remains in place and continues to function as normal. So you end up with two loans tied to the property.

Under the right circumstances, home equity loans can deliver the following benefits:

In Washington, home equity loans typically come with fixed interest rates. This means your monthly payments will remain the same throughout the loan term. This predictability can help with budgeting and financial planning.

Using a home equity loan, you could tap into your accumulated equity without altering your current mortgage terms. This can be beneficial if you currently have a low interest rate or other beneficial terms on your existing mortgage.

You can borrow a specific amount based on your needs and the available equity, without necessarily having to refinance your entire mortgage balance.

There are plenty of home equity loan and refinancing pros and cons to consider before settling on one particular option. The best way to choose between refinancing or a home equity loan is by considering your individual circumstances and long-term financial goals.Refinance might be a good option in the following scenarios:

In summary, you have choices when it comes to Washington home equity options; namely, a mortgage refinance or home equity loan. If your main goal is a lower rate or changing your term—and you’ll stay in your home long enough to cover closing costs—a refinance is usually the best choice.

If you just need to tap some equity quickly, keep your favorable existing rate, and don’t want to shuffle your entire mortgage, a home equity loan might make more sense.

If you’re looking to buy in Washington, we can help. At Sammamish Mortgage, we offer various mortgage options for you to choose from. Visit our website to get an instant rate quote or call us today to have your mortgage questions answered!

Whether you’re buying a home or ready to refinance, our professionals can help.

{hours_open} - {hours_closed} Pacific

No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.