No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.

In California, mortgage insurance is often required when a home buyer makes a small down payment—a smaller down payment results in a higher loan-to-value ratio, which can require the borrower to pay.

This article is an educational resource for California home buyers and homeowners who have questions about this subject. Below, we have answered some of the most common questions about California mortgage insurance, including costs, requirements, and other key topics.

Mortgage insurance is a unique insurance coverage that protects mortgage lenders from losses relating to borrower default. In this context, a “default” occurs when a homeowner stops making monthly mortgage payments.

While the policy itself protects the lender, it’s the borrower who pays for mortgage insurance. This is true for both conventional and government-backed home loans.

Mortgage insurance is an industry-wide standard rather than a government-imposed law. And it’s not required for all mortgage loans. California home buyers who make larger down payments can avoid the extra cost of mortgage insurance.

For conventional home loans not backed by the federal government, private mortgage insurance is typically required when the loan-to-value ratio rises above 80%. This means a home buyer with a single mortgage loan with a down payment below 20% will probably have to pay private mortgage insurance in California.

The rules are different for FHA-insured home loans. All borrowers who use this program have to pay mortgage insurance.

Get the latest updates right to your inbox

The cost of mortgage insurance in California can vary depending on whether it’s private or government-provided.

PMI: The average mortgage insurance in California for conventional loans ranges from 0.58% to 1.86% of the loan amount per year, according to data from the Urban Institute’s Housing Finance Policy Center.

This is specifically for Private Mortgage Insurance (PMI), a type of mortgage insurance you would have to pay if you take out a conventional mortgage with a down payment of less than 20% of the purchase price. The cost can vary based on the borrower’s credit score, the loan-to-value ratio, and other factors.

FHA: There are two types of premiums applied to FHA loans. An upfront premium typically equals 1.75% of the base loan amount, along with an annual premium that can vary based on several factors. Most home buyers in California who use FHA loans have an annual premium of 0.55% of the loan amount.

Using an example, let’s illustrate how much you can expect to pay for PMI.

The lender calculates monthly PMI payments by multiplying the loan amount by the PMI rate and then dividing by 12. For instance, the loan amount is $500,000, and the PMI rate is 1.50%. Remember that PMI rates vary based on credit score and other factors.

In this situation, your monthly PMI payments would be $625. The calculation to arrive at this figure would be as follows:

This additional $625 would be added to your monthly mortgage payments.

You can reduce the amount you pay in PMI payments by increasing your down payment. The more money you put toward your home loan, the lower the mortgage insurance rates in California. And if possible, making a down payment of at least 20% will help you avoid mortgage insurance in California altogether.

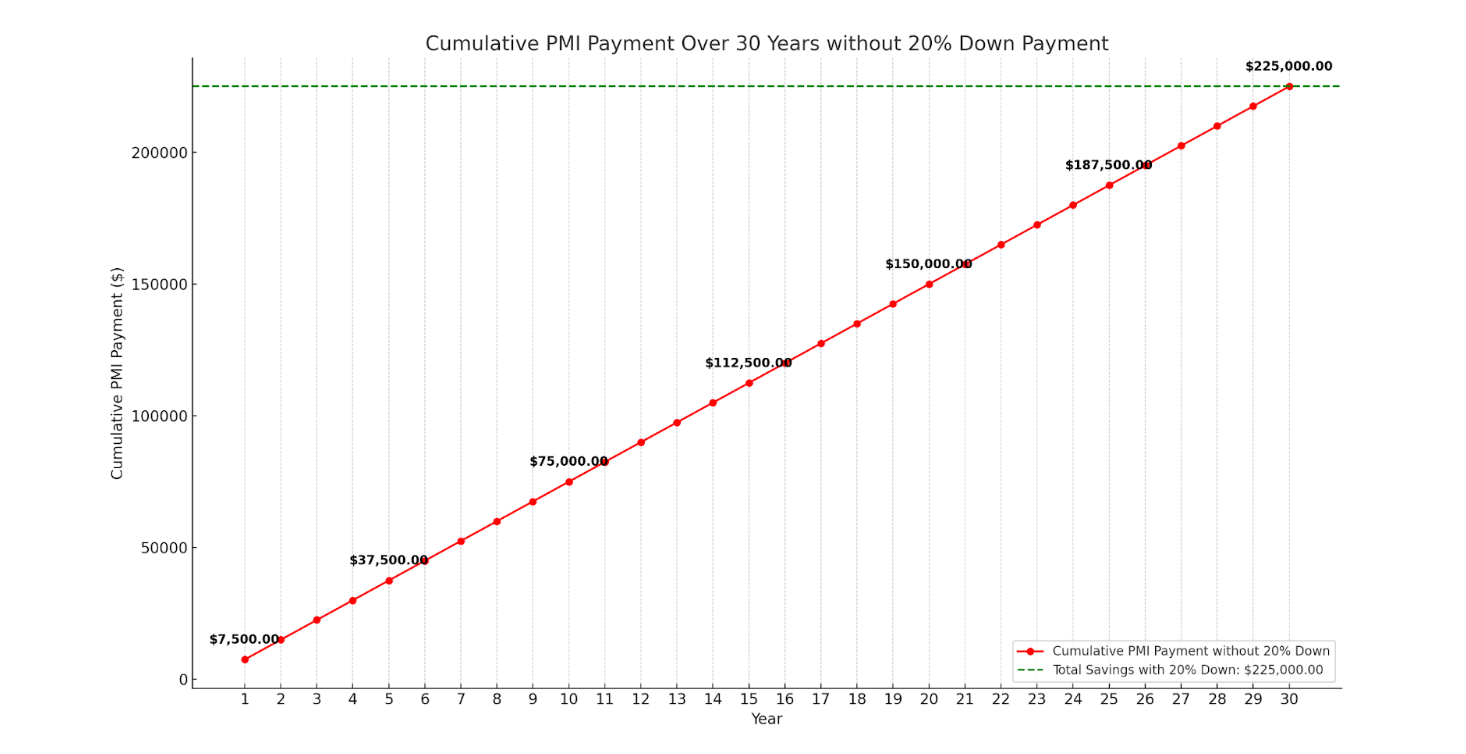

Here’s a line graph illustrating the cumulative PMI payments over 30 years for borrowers who don’t make a 20% down payment:

The red line with markers indicates the cumulative PMI payment each year. As you can see, the amount steadily rises, reaching $225,000 by the end of 30 years.

The green dashed line represents the total savings a borrower would have if they put down 20% initially. This equates to a significant $225,000 savings over 30 years.

By displaying the cumulative payment year-by-year, borrowers can understand the long-term financial implications of not making a 20% down payment. Putting down 20% upfront can result in substantial savings in the long run.

Home buyers in California often view mortgage insurance as an unwanted expense, something to be avoided whenever possible. And that’s understandable. After all, it does increase the size of your monthly loan payments.

But it also provides a major advantage to home buyers. Mortgage insurance allows you to buy a home sooner rather than later. Without this protection, mortgage lenders would likely require much larger down payments.

These days, a home buyer in California can make a down payment in the 3% range. But that’s partly because of the mortgage insurance industry. Most home buyers would have to make larger down payments if it weren’t for PMI and FHA mortgage insurance.

Homeowners and mortgage insurance are two entirely different things, though sometimes confusing.

As mentioned above, California mortgage insurance policies protect the lender who is funding the loan. On the other hand, a homeowners insurance policy protects the person who owns the home.

Homeowners insurance protects your home and its contents from damage caused by covered events like fire, wind, hail, theft, and vandalism. It can also provide liability coverage in case someone is injured on your property or you accidentally damage someone else’s property.

The state of California does not require homeowners insurance by law. But if you use a mortgage loan to finance your home purchase, your lender will probably require you to have at least a basic home insurance policy before closing.

As a home buyer in California, you could avoid paying mortgage insurance in several ways. Here are the three most common strategies:

Use a conventional loan with a down payment of 20% or more. If you do this, your loan-to-value ratio will not exceed 80%. That means you’ll avoid the “trigger” that requires California private mortgage insurance on a conventional loan.

Combine two mortgage loans in a “piggyback” fashion. If you can’t afford to make a 20% down payment, you could combine two mortgage loans so that neither has an LTV above 80%. For instance, a borrower could use the 80-15-5 strategy.

This is where one mortgage loan covers 80% of the purchase price, a second loan covers an additional 15%, and the borrower pays the remaining 5% as a down payment.

Use a VA loan to buy a house in California. The VA home loan program is available to many military members and veterans in California. It offers several benefits, including buying a house with no down payment. Mortgage insurance is not required for VA loans.

In California, private mortgage insurance is not permanent. Homeowners can cancel their PMI once they have reached a certain level of equity in the home.

Over time, as a homeowner makes their regularly scheduled mortgage payments, their equity or ownership level increases. When a person reaches the 80% equity level, their loan-to-value ratio has dropped below 20%. So, PMI would no longer be needed.

When the LTV ratio drops to 80%, California homeowners can ask their loan servicers to cancel the PMI policy. When the LTV drops to 78%, it should trigger an automatic cancellation. But being proactive and communicating directly with your loan servicer never hurts.

Considering this, ensuring that the home you intend to buy will appreciate at a healthy rate would be prudent. For instance, some areas may have a higher appreciation rate in property values than others. In other cases, you may consider updating the home to add instant value and equity to the home.

Again, once the home’s value has increased to an amount that brings your loan-to-value ratio under 80%, some lenders may let you request to cancel your mortgage insurance. However, remember that your home will likely have to be appraised for the lender to verify its current value before dropping your PMI.

Consider a refinance. You can also refinance your mortgage to remove California private mortgage insurance. Refinancing involves taking out a new mortgage with different terms and rates and using the funds from the new loan to repay the existing loan.

Many homeowners choose refinancing to tap into their home equity to help cover the cost of a big expense. But others way choose refinancing as a way to get rid of their mortgage insurance.

For instance, if you initially took out a mortgage with a 10% down payment, refinancing your mortgage to a loan with a higher equity share once your home equity reaches 20%. This would remove the PMI.

FYI: A “loan servicer” is a company responsible for managing the day-to-day administrative tasks of your mortgage, including collecting your monthly payments, managing escrow accounts (if applicable), and providing customer service.

If you’re looking to buy in California, we can help. At Sammamish Mortgage, we offer various mortgage options for you to choose from. Visit our website to get an instant rate quote or call us today to have your mortgage questions answered!

Whether you’re buying a home or ready to refinance, our professionals can help.

{hours_open} - {hours_closed} Pacific

No Obligation and transparency 24/7. Instantly compare live rates and costs from our network of lenders across the country. Real-time accurate rates and closing costs for a variety of loan programs custom to your specific situation.